Airlie Australian Share Fund Investor Letter

Download Combined Letter & Factsheet (PDF)

Download Combined Letter & Factsheet (PDF)

It was another strong year for markets, with the ASX 200 returning 12.1% for the year, on top of last year’s return of 14.8%. The Airlie Australian Share Fund (“AASF”) returned 12.44% for the year (net of fees), outperforming the index by 0.34%.

The story of the year was the performance of the banks, with the Big Four banks delivering c50% of the total index return for the year. While it was pleasing for us to slightly outperform in such a market, given our substantial underweight to the Big Four (we own CBA and NAB, with our banks weighting now half the total major banks’ weighting in the index), this annual result included a disappointing fourth quarter of performance for us, with the AASF falling 4.8% in Q4, well below the ASX 200 fall of -1.05% during the same period.

Five portfolio holdings really went against us this last quarter: Mineral Resources (-24%), Ampol (-19%), James Hardie (-23%), Charter Hall (-17%) and Orora (-23%). We believe the first four of these present us with an opportunity to add to our existing holdings at more attractive prices. Stepping through each:

-

Mineral Resources (ASX: MIN) fell as the lithium price correction has been sharper than expected with the price of spodumene hovering around US$1,000/t today. At these prices we believe the vast majority of producers are cash flow negative, which has weighted on investor sentiment towards the lithium sector. For example, former lithium high flyer Liontown (-30%, not held) was the worst-performing stock in the ASX 200 in FY24. We believe Mineral Resources is better positioned than its lithium peers given its low-cost producing status and most importantly the diversified nature of its operations. We estimate iron ore and mining services will account for 78% of group earnings in FY25. In our view, the combination of earnings growth and balance sheet deleveraging should see the share price re-rate higher over the next 12 months.

-

Ampol (ASX: ALD) had a poor quarter following its quarterly update in April driven by weaker refining margins that are a result of concerns over new global refining supply ramping up this year. Overall, we remain optimistic about the fundamental outlook of the global refining sector, possibly one of the most underfunded in the energy complex. Elsewhere for Ampol, jet fuel volumes continue to recover; a rational domestic environment supports fuel margins; and we’re seeing upside from a rebooted retail strategy. These upsides leave us positively disposed to the company. Additionally, management has not put a foot wrong with capital allocation and so barring the purchase of the EG Group collection of retail sites, we expect continued special dividends, putting the company on a 7% dividend yield, fully franked.

-

James Hardie (ASX: JHX) downgraded expectations for FY25 earnings following the Q4 result, largely as a function of continued softness in North American repair and remodelling spending. Higher mortgage rates have slowed US housing market activity, and James Hardie as a manufacturer of fibre cement siding is not immune. What has not changed is the long-term structural opportunity for James Hardie in North America – to continue taking share in a growing market where housing is undersupplied. Our view here was strengthened at the company's recent North American investor day, which we attended. We believe that the through-the-cycle return on capital for James Hardie is fantastic (>25%), the balance sheet is strong (<1x leverage) and management is high quality. We have been adding to the position on weakness and consider the company to be a core long-term holding in the portfolio.

-

Charter Hall (ASX: CHC) fell despite the office market unlocking somewhat with transactions at levels of better-than-implied valuations. The narrative of higher interest rates post the May inflation print, however, produces near-term headwinds to AUM growth, resulting in devaluations as well as reduced transaction activity as buyers and sellers wait for rates to peak to know when to transact. There is uncertainty on how long it could take for these factors to resolve. However, our view is that Charter Hall is fundamentally cheap at 14.9x FY24 EPS guidance (vs ~17x historical average); we believe FY24 represents trough earnings as it consists mostly of the recurring fee streams and has minimal transaction and performance fees. While there are valid concerns about the Office sector more broadly, we would note it accounts for ~33% of Charter Hall overall FUM with the balance allocated to Industrial and Logistics (~31%), Retail (~13%), Listed Equities (~19%), and Social Infrastructure (~4%).

While we have topped up the above positions, Orora (ASX: ORA) is a different story, a painful mistake for us that we have decided to exit. In November 2023 Orora completed the acquisition of French premium spirit bottle producer Saverglass. Since then, the company has downgraded earnings expectations for Saverglass twice, and also highlighted weak trading conditions in the North American packaging distribution segment. For Saverglass, the earnings downgrades have come as a result of the global slowdown in consumer spending and a subsequent destocking of spirits globally. The obvious frustration is these earnings downgrades imply Orora has paid the wrong price for Saverglass and in their due diligence failed to adjust their offer price for any potential cyclical risks. The stock has de-rated significantly since the acquisition as a result. Our own research indicates Saverglass is a good business that is well invested and has a strong market position. Given this view, we would generally be happy to lean into cyclical weakness and buy more stock. However, in this instance ORA has taken on material debt to pay for the acquisition. With net debt to EBITDA at c2.8x on our estimates, we believe the company has the wrong financial structure for the cyclicality of its business model, and hence now fails our financial strength test. While we exited our position in April, we keep a watching brief on the situation; the share price has fallen another 12%, and a willingness to explore asset sales may address our balance sheet concerns.

Outlook and positioning: expectations are everything

This time last year, consumer confidence was at 1991 recession-type levels, retailers were downgrading every week, we had worn 12 interest rate hikes in a row and Macquarie Dictionary declared “cozzie livs” (slang for cost of living) as its word of the year. Roll forward to today: consumer confidence has not budged, interest rates have increased another 25bp, retailers are downgrading again and the cost of living crisis has gotten so bad that the Liberal Party, historically the party that is pro-business and anti-government intervention, is arguing for divestiture powers over the supermarkets as a way to alleviate cost-of-living pressures.

Against this backdrop, it might be surprising to note that three of the best-performing sectors for the ASX 200 this year were Consumer Discretionary (+23%), Financial Services (banks) (+29%) and Real Estate (REITs +21%). While we were blindsided by the degree of re-rating in the banks, we were unsurprised that consumer discretionary and REITs performed so well against this tough backdrop. It all comes down to expectations. As we noted in our investor letter last year: “We are starting to see bearish, even very bearish, expectations being priced into the consumer-facing parts of the Aussie economy.” This environment provided an excellent buying opportunity as some of these stocks, including portfolio holdings Premier Investments and Nick Scali, had phenomenal balance sheets that could more than withstand an economic slowdown. These two businesses alone are both up c60% over the year, despite the fact the economy has indeed slowed down, with GDP growth slowing from 0.4% last June quarter to 0.1% in the most recent March quarter. It was another good reminder that if the balance sheet of a business is good, the lower the share price, the lower the risk.

Subsequently, the share prices of these stocks have risen as a function of earnings expectations rising from these bearish lows and PE multiple expansion. For example, in June 2023, the majority were forecasting FY24 EPS of $1.55 for Premier, and the shares were trading at 12.6x these expectations. Fast forward to today, the expectation is $1.72 EPS to be delivered at the FY24 results in September, and shares are trading at 17x those expectations. In response to this increase in expectations, we have halved AASF’s position in Premier at current levels, as well as reducing AASF’s position in Nick Scali and Wesfarmers. While all three remain core portfolio holdings, we believe the increase in expectations has changed the risk/reward proposition.

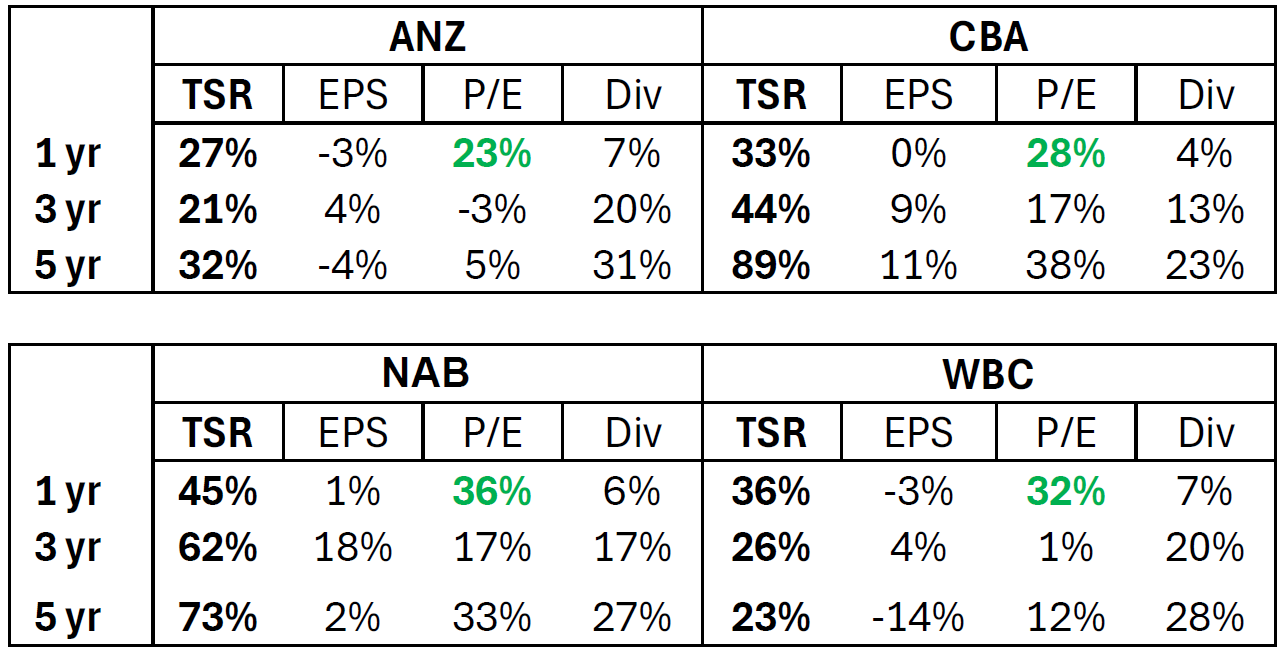

While the performance of these retail stocks was driven by a combination of higher earnings and a multiple re-rate, the extraordinary performance of the Big Four banks this year was driven primarily by a re-rate. As per the figure below, the bulk of the total shareholder return for the Big Four over the last five years has come in the last year (with the exception of CBA, which has been a solid performer over one, three and five years). Within that, the bulk of the 27-45% TSR the banks enjoyed this year was driven by the P/E multiple re-rating. This tells us that expectations have increased dramatically for the banks. We have owned CBA and NAB in the portfolio since inception yet have reduced our holdings in both this year to reflect these heightened expectations, and are now AASF is as “underweight” in the Big Four as we’ve ever been.

Fig 1: Total shareholder return (TSR) composition for Australian banks

Source: Macquarie Research

A year ago, the gloomy outlook for the economy meant investors were more than willing to hide in expensive defensives. Ironically, these proved to be the riskier end of the market over the next 12 months. In June 2023, the Woolworths share price was $39.50 with the consensus expecting Woolworths to deliver FY24 EPS of $1.52, and shares were trading at 26x those forecasts. After a bruising few months in the headlines during the supermarket inquiry into pricing practices, Woolworths delivered a disappointing 3Q24 sales update in May, driving consensus to downgrade FY24 EPS expectations to $1.40, and the stock traded at 22x on those lowered expectations, at a share price of $30.30.

A year ago Telstra was riding high at $4.35, expected to deliver 19c EPS and was trading at 26x. Today Telstra is forecast to deliver 17c and is trading on 22x, at a share price of $3.71. Clearly the expectations were too high for both businesses, and the multiple that investors were willing to pay was also too high.

While the low historic ROIC profile of Telstra remains uncompelling to us despite the de-rate, we added Woolworths to the portfolio in May.

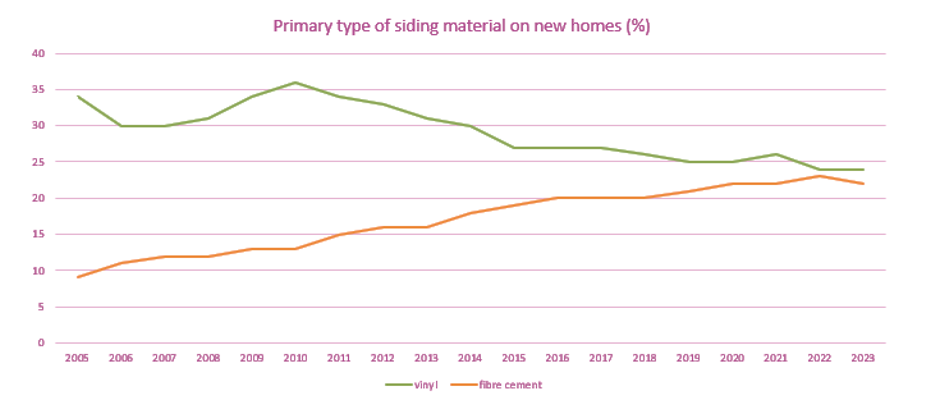

We also see depressed expectations for the North American housing cycle as a great opportunity to add to our position in James Hardie. We recently returned from the US, attending the James Hardie North American investor tour, as well as meeting with contractors, dealers, builders and market forecasters to understand the dynamics of the US housing market and Hardie’s ability to continue gaining share in siding.

As per the below chart, fibre cement (a category for which James Hardie has 90% market share) has been taking share from vinyl siding as the primary type of siding that people put on their homes in the US. Our meetings affirmed our expectations for these share gains to continue for a simple reason: fibre cement siding looks so much better than vinyl. Vinyl is cheap, plastic and warps/cracks easily.

Source: US Census data, Airlie research

The only thing vinyl has going for it over fibre cement is price: total on-the-wall cost for siding a typical house in fibre cement might be c$40k, whereas vinyl would cost c80% of that. As house prices have risen over time, we believe fewer people will be willing to reside in houses with vinyl.

Further, the trip highlighted the extent of the “lock-in” effect, with homeowners unwilling to tap into the mountain of home equity they are sitting on, because 30-year mortgage rates have gone from having a 2-handle to over 7%. Many market participants felt it would take a rate cut (or several) to get this “repair and remodel” part of the market moving again. However, once it is moving the uptick in activity could be enormous: one market participant pointed out to us that the homeowner wealth created via rising house prices in the last five years is US $12 trillion, which is 2x the amount of homeowner wealth that was destroyed during the GFC. As such, the recent downgrade and subsequent 17% share price fall in James Hardie offers a good buying opportunity, in our view, as expectations are now clearly lower, while the long-term fundamentals look solid.

Emma Fisher, Portfolio Manager

Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management (‘Airlie’). This material is issued by Airlie and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any fund, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Further information regarding any benchmark referred to herein can be found at www.airliefundsmanagement.com.au/benchmark-information/. Any third-party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie.